In two articles published in January 2023 and in March 2023 Yuemei Ji and Paul De Grauwe pointed out that the ECB is subsidizing commercial banks massively against inflation, which may represent a more than €1 trillion transfer of money from taxpayers to private banks over the next ten years. The authors further claim that such subsidies are exorbitant, unjustified, and evitable as these can be addressed or at least mitigated by raising minimum reserve requirements (more on this below).

The article underlines that quantitative easing operations undertaken by major central banks have created a regime where central banks have supplied to banks, in exchange of the securities purchased, abundant reserves that outpace by far the demand for such reserves. As a consequence, central banks need to remunerate these reserves so as to maintain a control on overnight rates as otherwise banks would lend such costless overabundant reserves at levels tending to zero. In which case central banks will not be in a capacity to determine short-term interest rates.

Yi and De Grauwe, provide a straightforward scenario-based calculation of the estimated aggregate amounts that are expected to be transferred by the eurosystem for the year 2023 to the banks by means of such remunerated reserves. In February 2023, bank reserves in the eurosystem amounted to €4.3 trillion. If effective rates applied for reserves for the last three quarters of 2023 are of 3.5%, such transfers would amount to €151 billion euros, an amount roughly equivalent to expenditures under the annual EU budget . (N.B. It is to be noted that current rates (as of July 2023) applied to the deposit facility are of 3.75%).

Interestingly, such remuneration policy means that in practice such transfers would in 2023 offset the net decline of size of the eurosystem balance sheet pursuant to the discontinuation of net asset purchases under the ECB’s Asset Purchase Programme (APP).

Even if rates decline so as to reach an compounded level of 3% From April to December 2023 (which by the way seems very unlikely as the ECB ha committed to continue increasing rates to fight inflation), the transfer would still be of €129 billion.

The authors then assume that rates may remain at around 3% for the foreseeable future (which is in line with market expectations). They also assume that the ECB will reduce the size of the eurosystem balance sheet by €15 billion per month. In such case the amounts transferred to banks by the ECB would amount to €1047 billion over the next ten year.

Yi and De Grauwe underline that by remunerating reserves, the ECB is in practice transferring to the banking sector the profits it generates by means of its monopoly on euro denominated central bank reserves that represent the ultimate means of settlement between banks. Such transfers have also the consequence of transforming the maturity of public debt by transforming long-term government debt into short-term debt:

« Most of the government bonds held by the Eurosystem (and other major central banks) have been issued at very low interest rates, often even zero or negative. This implies that governments are immune for some time from the interest rate rises. By paying an interest rate of 2% on bank reserves and thus reducing government revenues in the same amount, the central bank now transforms this long-term debt into highly liquid debt forcing an immediate increase in interest payments on the consolidated debt of the government and the central bank ».

The authors point out that such public transfers to banks can and should be avoided by means of increased compulsory reserves. In the first article they propose to raise minimum reserve requirements from 1% of deposits as it is the case today, so that the amount of excess reserves for which supply outpace demand become compulsory reserves on which no interest would be paid. By doing so, the ECB would be able to continue setting overnight interest rates while avoiding the above-mentioned transfers. In practice such level of compulsory reserves requirement would mean a de facto return to a reserve scarcity regime that prevailed before the financial crisis where supply did not outpace demand. The authors therefore clam that such massive transfers can therefore easily be avoided, while preserving the capacity of the ECB to set short term interest rates.

In their first article Yi and De Grauwe are aware that their proposal would be perceived as ‘quite intrusive’ and will be resisted by the banks, which will see an easy source of profit disappear at once. It is likely to be resisted by central banks also because it implies a return to operating procedures that existed in a reserve scarcity regime prior to the financial crisis ». In a nutshell, they rise the hypothesis that:

« (…) It could also be, of course, that central banks make these large transfers to banks out of a concern that the recent interest rate increases make banks more vulnerable. It is indeed the case that when interest rates increase banks’ profits tend to decline, because their liabilities have a shorter maturity than their assets. An interest rate increase is transmitted faster to the liabilities than to the assets, leading to a decline in banks’ profits. By remunerating bank reserves, central banks solve this problem of commercial banks at the expense of their own profits. »

Yi and De Grauwe push further the argumentation in their second article by pointing out that even if one accepts for the sake of the argument that there may be good reasons for sticking to a floor system and avoid coming back to a framework of reserve scarcity, it is still possible to device a system that would still avoid making massive public transfers to the banking sector while maintaining the floor-based current operating procedure by means of a two-tier system. Such system would impose non-interest bearing compulsory deposit only « on part of the bank reserves. The bank reserves exceeding the minimum requirement (excess reserves) would then be remunerated as they are today » If for instance, non-remunerated compulsory reserves would cover 75% of reserves above demand, the transfer will amount to only 1/4 of the ongoing transfers while still keeping a floor-based regime of abundant reserves (see table above).

The second article raises therefore two fundamental question: why is such a floor system an instrumental feature for monetary policy and therefore what are the impediments for reverting to the status quo ante of scarce reserves? Furthermore, at what point do reserves become abundant or scarce?

As outlined in the previous post of this blog, central banks may see such ‘floor system’ operational framework as a key element of an overall policy framework aiming a reconciling price stability and financial stability. The bet is that such reconciliation may be achieved by using their balance so as to perform a market maker function for public and private bonds and money markets, and thereby to ensure the ‘derisking’ provision of safe and liquid assets to the banking sector while using interest rates on the deposit facility to address price stability. As hinted by Yi and De Grauwe, a blunt way of squaring the circle of achieving both price and financial stability is therefore to directly contribute to bank profitability while keep using short-term interest rates to address inflation. As also indicated in our previous post, the low profitability of the euro area banking system is indeed a reason of concern for the ECB since several years as the institution claims it hampers its monetary transmission channel.

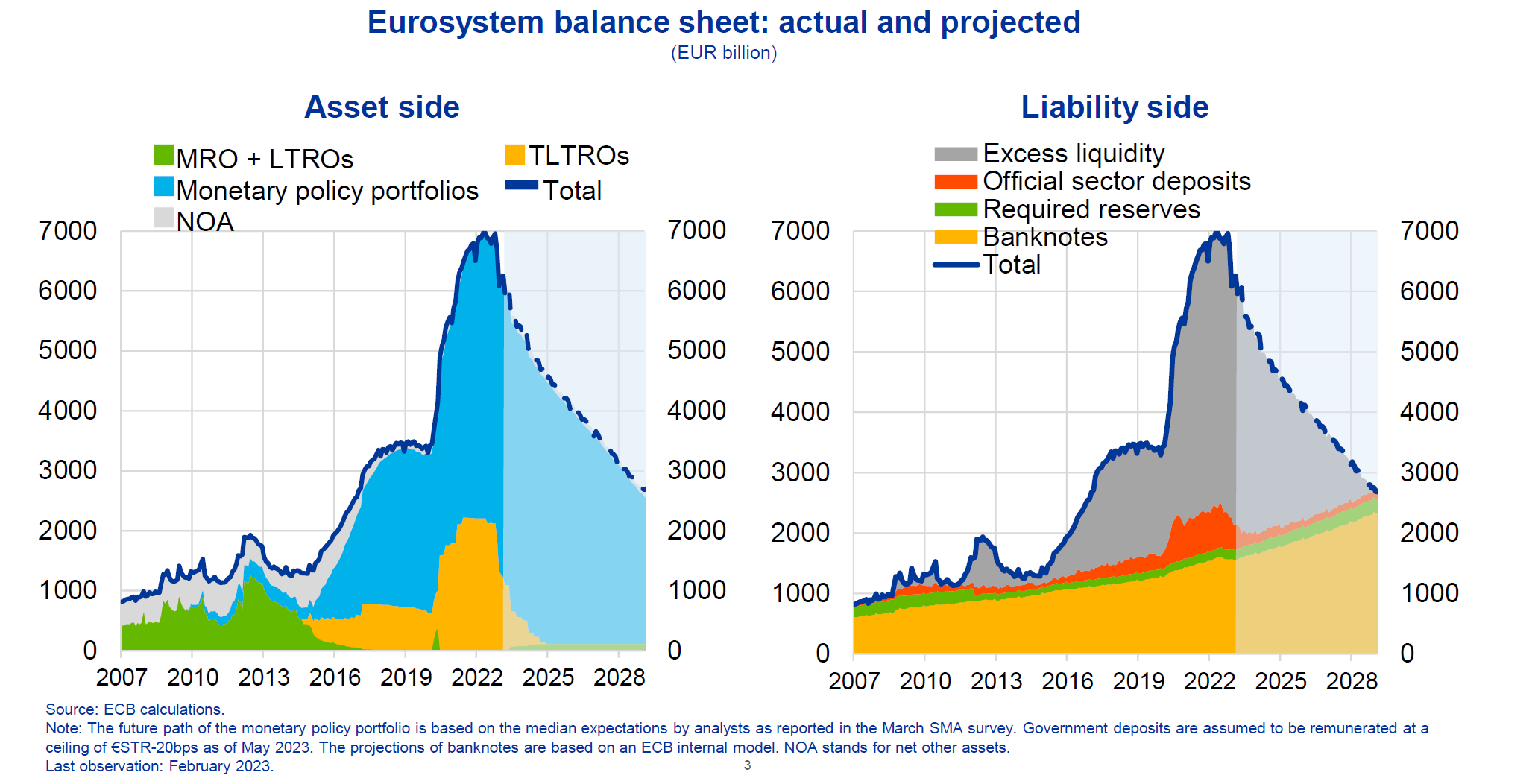

Before exploring additional elements of answer answers to the above-mentioned questions, it is also important to note that despite the ongoing process of monetary tightening in which major central banks are engaged, reserves are expected remain overabundant in the foreseeable horizon as major central banks have shown clear indications that they intend to continue operating a ‘floor system’ and have also shown a high degree of flexibility for accommodating liquidity needs when they arise. The Bank of England injected for instance massive amounts of liquidity in October 2022, fully reverting previous quantitative tightening operations to quell concerns around pension funds and reduce Guilt yields. Similarly, in the middle of the banking turmoil of the first quarter of 2023, the US Fed injected, in only one week, an amount of liquidity (US dollar 300 billion) equivalent to the reserves withdrawn in the five previous months. As for the ECB, irrespective of its policy tightening, the institution has already outlined (as illustrated in the figures below) that it will continue caeteris paribus providing ample excess reserves, to the banking sector for the foreseeable future and at least until 2029.

In a speech given at the end of March 2023 at the Columbia University, Isabel Schnabel, member of the ECB’s executive board, provides a certain number of elements of answer to the questions above.

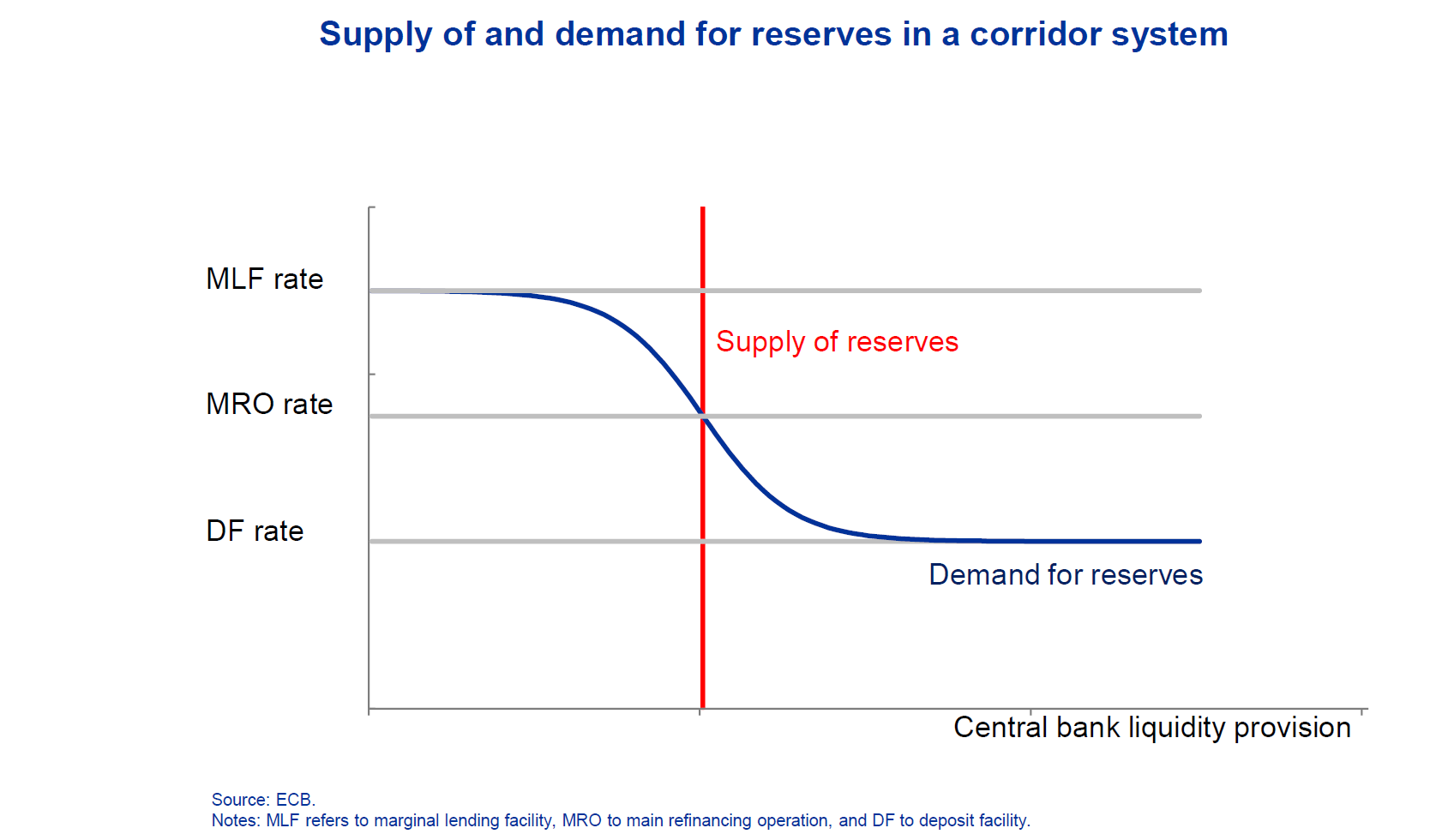

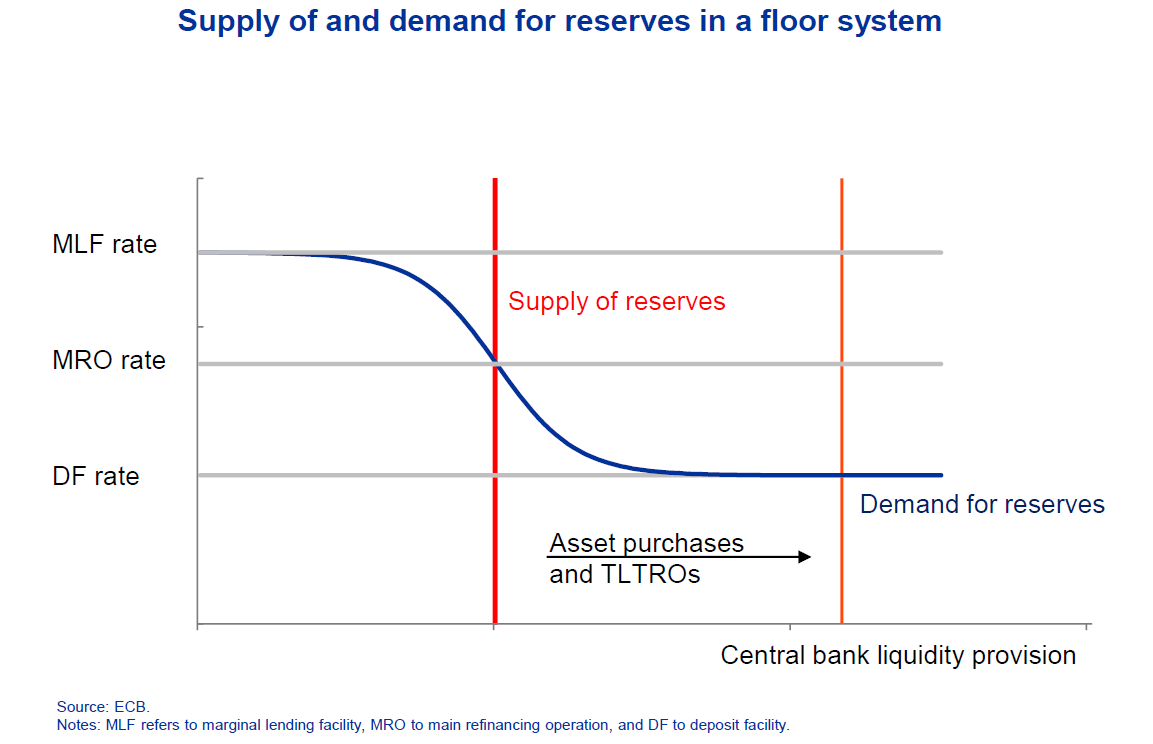

The speech underlines first the features determining the transition from a corridor that prevailed until the financial crisis to a floor system where reserves became overabundant due to unconventional policies such as asset purchases and targeted longer-term refinancing operations (TLTROs). The presentation provides in that respect a stylized graphic illustrating the way reserves supply and demand are modelled:

As it was the case before 2008, when the supply of reserves remains below the point of abundance where the curve becomes flat, the ECB implemented a corridor system according to which short-term rates were steered towards the main refinancing operation rate in the middle of the corridor. If reserves supplies become however overabundant, no bank would have incentives to lend short term liquidity to other bank below the ECB deposit facility rate as they can simply secure the rate of the deposit facility. Similarly, such supply cannot become too scarce, as otherwise banks would be undersupplied and would have a more systematic recourse to the more onerous marginal lending facility and thereby would not be able to borrow from each other below such rate. A corridor system where a central banks steers short-term rates towards the main refinancing operation rates in the middle of the corridor as the one that prevailed before the financial crisis can therefore only work when reserves were scarce (but not excessively scarce).Nevertheless, after 2008 there was a transition towards a floor system where the demand curve become flat and short-term rates have been determined by the deposit facility rate as it became clearly the case after 2014 when the ECB significantly incremented reserves by means asset purchases and broader refinancing operations.

As for the question on why did a floor system became such an instrumental feature for monetary policy as well as the question on what are the impediments for reverting to the status quo ante of scarce reserves, Schnabel provides some hints that point towards the environment that emerged after the financial crisis. She notably indicates (emphasis our) that:

« large excess reserves have blurred our understanding of banks’ underlying demand for liquidity. The aggregate level of reserves has been largely determined by the quantity of asset purchases rather than by banks’ liquidity choices ».

Despite such blurring, Schnabel claims there are good reasons for believing that such demand for liquidity may have structurally increased, meaning that the demand curve may have significantly shifted to the right.

« tighter financial regulation has made our financial system safer and more resilient, it has [also] made interbank lending more costly. Banks might also want to hold much higher liquidity buffers than in the past. »

In Schnabel’s view there are two main reasons for such higher demand for reserves (gain emphasis our) :

« One relates to regulatory changes. The introduction of Basel III has resulted in a measurable increase in the demand for high-quality liquid assets (HQLA) that banks need to hold to comply with the liquidity coverage ratio (LCR). Many euro area banks currently use excess reserves to meet regulatory requirements, especially in those countries with high excess liquidity. For the euro area as a whole, excess reserves currently account for 60% of HQLA holdings. The second factor relates to banks’ precautionary behavior in guarding against liquidity risks, as the turbulent events in the past few weeks forcefully underline« .

Schnabel refers here of course to the banking turmoil of the first quarter 2023. She also mentions in her speech the events in the autumn 2019 when « interest rate volatility spiked unexpectedly although the supply of reserves was still considerably above what banks had indicated in surveys as their lowest comfortable level. »

Therefore, as Schnabel indicates there are good reasons for believing that the demand for reserves may be significantly and structurally higher that in a pre-financial crisis world (I will come back to this issue in a next post). As for the question on the point at which reserves become scarce or abundant she also hints that due to the oversupply of the very same reserves following the expansion of asset purchases, that has blurred central bank’s understanding of the underlying demand for liquidity, there is a high level of uncertainty as regards the ‘kink’ point where the demand curve for reserves becomes steep and sudden and severe pressures on interests rates may appear. Such reasoning seems therefore to provide elements of justification on why the ECB does not seem ready to consider a genuine two-tier system where a meaningful part of excess reserves would be subject to non-remunerated compulsory requirements. I use here the word ‘genuine’ as the ECB has indeed decided in July 2023 that compulsory reserves will not be remunerated anymore. However, the level of compulsory reserves as currently set out by the ECB are only a small fraction of excess reserves. Interestingly, the ECB has justified such a move by indicating that:

[such] decision will preserve the effectiveness of monetary policy by maintaining the current degree of control over the monetary policy stance and ensuring the full pass-through of the interest rate decisions to money markets. At the same time, it will improve the efficiency of monetary policy by reducing the overall amount of interest that needs to be paid on reserves in order to implement the appropriate stance.”

As pointed out however by Mayrick Chapman, the annualized costs minimum reserves cost the ECB EUR 5.5 billion per year in interest, while the Deposit facility cost EUR 127 billion per year. As the ECB increased interests rates by 25 basis points also in July 2023. Therefore, the aggregate effect of July 2023 decisions is that an increase in interest paid by the ECB (and its members) to the Euro-zone banking system of EUR 4.3 billion on an annualized basis. This leads Chapman to wonder what is meant when the ECB says that the minimum reserve decision ‘will improve the efficiency of monetary policy by reducing the overall amount of interest that needs to be paid on reserves’…

Self-induced uncertainty as a collateral effect and ‘overflow’ of monetary policy itself becomes therefore a reason for avoiding having to find out where is the abundancy/scarcity boundary, and therefore provides expediency for justifying a floor regime of abundant reserves that entails large transfers to the banking sector.

Interestingly, the US Fed that is confronted with a similar debate has coined a new concept to refer to such boundary between scarcity and abundance: the Lowest confortable level of reserves (LCLOR) for the US economy. It has estimated such threshold at around 2.2 trillion US dollars. Such estimations are based on different methods and extrapolations built notably on the levels that prevailed before money market experienced severe turmoil in the autumn 2019, in a context where the FED was reducing the amount of reserves. Albeit the Fed has in contrast with the ECB provided estimations of such boundary threshold and as pointed out by Joseph Wang such estimations remain however subject to a high level of uncertainty and in any case the Fed may be too afraid to find out in practice…

To use a metaphor the whole justification of a floor system that transfer vast amounts of resources to the banking sector sounds as if central banks were telling us: ‘we have fed a beast somewhere there in the forest, but we don’t really know how dangerous or big it is, although we have indications that it is indeed quite dangerous… so better not to find out and continue feeding it, as otherwise it may show up… (I will come back to that metaphor in a subsequent post as well).